Both 401K vs IRA have precious tax blessings, and you may make contributions to each at an equal time. The most important distinction between 401(k)s and IRAs is that employers provide 401(k)s, however people open IRAs (the use of agents or banks). IRAs normally provide extra investments; 401(k)s permit better annual contributions.

If the 401(k) vs IRA contrast is weighing on you, here’s the fast answer:

-

If your company gives a 401(k) with an agency fit: Consider placing sufficient cash on your 401(k) to get the best. That fit might also additionally provide a 100% go back to your cash, relying on the 401(k). For example, a few employers promise a 100% fit as much as 3% of profits. In that manner, in case your profits are $50,000, your company will be positioned at $1,500, so long as you furthermore might make contributions of at least $1,500. Once you get the fit, then recollect maxing out an IRA for the 12 months, go back to the 401(k) and resume contributions there.

-

If your company doesn’t provide an agency fit: Consider skipping the 401(k) at the start and begin with an IRA or Roth IRA. You’ll get entry to a massive choice of investments whilst you open your IRA at a broker, and you will keep away from the executive charges that a few 401(k)s charge. After contributing as much as the IRA limit, consider investing your 401(k) for the pre-tax advantage it gives. Here’s how and where to open an IRA. (Wondering which IRA is fine for you? Here’s a way to select between a Roth IRA and a Traditional IRA.)

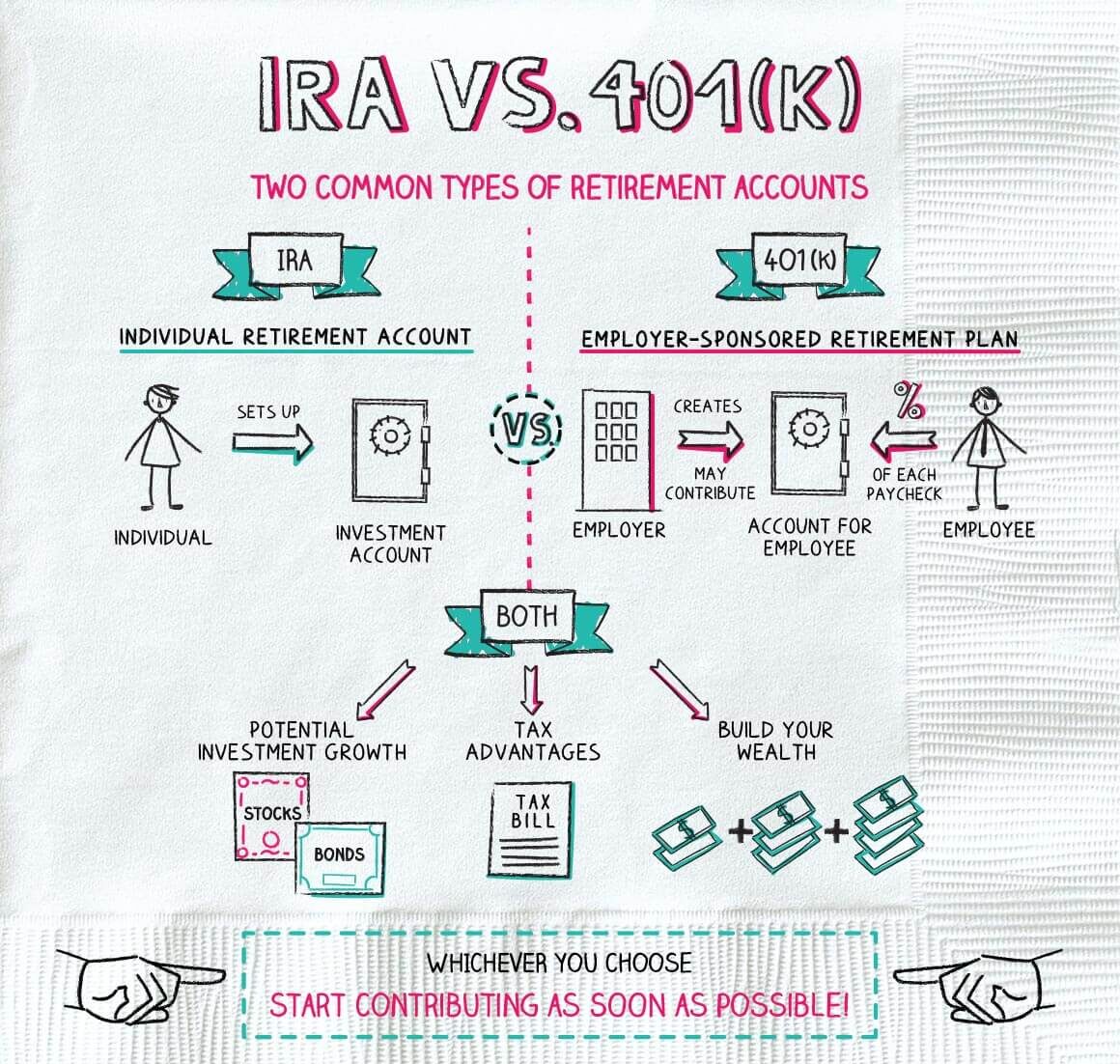

ira vs 401k

401k vs IRA: A street map

Hats off to you when you have the manner to max out each a 401(k) and a conventional IRA or Roth IRA. If now no longer, this IRA vs. 401(k) street map will assist you to prioritize your dollars.

Your first step relies upon whether or not your company suits your contributions in your place of work financial savings account.

If your company gives a 401(k) fit

Contribute sufficient to earn the whole fit. Check your worker blessings handbook. If you spot that your company suits any part of the cash you make contributions to the agency 401(k) plan, do now no longer skip this possibility to acquire your loose cash.

An agency matching application is one of all the largest blessings of a 401(k). In a manner that your company contributes cash in your account primarily based totally on the quantity of cash, you keep, as much as a limit. A not unusual place association is for a company to fit a part of the quantity you keep as much as the primary 6% of your earnings.

Even if a 401(k) has restricted funding picks or better-than-common charges, carve out sufficient cash out of your paycheck to get the whole agency fit, as it’s efficaciously an assured go back on the one’s dollars. Also notice that company contributions don’t be counted number closer to the 401(k) annual contribution limit.

Next, make contributions as tons as you’re allowed to an IRA. Depending on which sort of IRA you select — Roth or conventional — you may get your tax spoil now or down the street whilst you begin retreating finances for retirement.

-

A conventional IRA is good for folks who choose a direct tax spoil. Contributions can be deductible — which means your taxable earnings for the 12 months could be decreased via way of means of the quantity of your contribution. But, in case you’re additionally blanketed via way of means of a 401(k), your deduction can be decreased or removed primarily based totally on earnings. If you (or your spouse) have a place of work retirement plan, test out the IRA limits.

-

A Roth IRA is a great desire in case you’re now no longer eligible to deduct conventional IRA contributions, or in case you do not thoughts giving up the IRA’s on the spot tax deduction in change for a tax-loose increase to your investments and tax-loose withdrawals in retirement. Roth IRA eligibility isn’t always stricken by participation in a 401(k), however, there are earnings limits. You can see the present-day Roth guidelines on our IRA limits page.

Related – Useful recommendations for purchasing a foreclosed belongings